U.S. public companies seeking additional liquidity are increasingly looking to raise capital through equity lines of credit. Under an equity line of credit, a publicly listed company contracts with an institutional investor for the right to sell up to a specified dollar amount of common stock to the investor from time to time during an agreed-upon period of time. The company has the ability to draw on the equity line as if it was a revolving credit facility or an equity ATM program. The shares of common stock are privately placed to the institutional investor but registered for public resale on a shelf registration statement so that the investor has immediate liquidity with respect to the shares purchased. The purchase price for the shares purchased pursuant to the equity line of credit is typically calculated utilizing the market price of the company’s shares during an agreed pricing period following delivery of a notice to the investor, less a discount that was previously agreed to by the investor and the company.

The transactions generally have the following key terms:

- Available Amount: Generally $15 million to $350 million

- Duration: 36 months (sometimes 24 or 18 months)

- Determination of Purchase Price: The purchase price is generally a discount of 3-6% to the volume weighted average price (VWAP) of the company’s common stock over a period of 1-3 business days after delivery by the company of a drawdown notice to the investor.

- Minimum Acceptable Price: The company may specify a minimum acceptable price in connection with drawdown notice, but is not required to do so.

- Investor Fee: The investor typically receives a fee in cash or stock upon signing the equity purchase agreement. Fees vary but recent deals have had fees ranging from 1-2%. The investor also typically receives a small expense reimbursement (eg, up to $50,000).

- Registration Statement or Prospectus Supplement: If the company does not have an effective registration statement on file available for registering the investor’s shares, typically the company must file a new registration statement on Form S-1, S-3, F-1 or F-3 within a specified period of time after execution of the equity purchase agreement (eg, 30 or 60 days). The company must also cause the registration statement to become effective as promptly as practicable (some deals impose a 90 day deadline, and some impose a deadline of 10 business days after notice that the registration statement is not subject to SEC review). The registration statement must be effective before the company can draw down on the equity line. If the company already has an effective registration statement on file available for registering the investor’s shares, then typically the company will be required to file a prospectus supplement describing the transaction prior to commencement of sales.

- Representations. The company makes a full suite of representations and warranties about its business and its SEC disclosure.

- Short Sales: The investor will typically represent that it does not have a net short position in the common stock and covenant that it will not enter into or effect any short sales of the company’s common stock.

In addition, the equity purchase agreements typically provide that the ability of the company to draw on the equity line of credit is subject to some or all of the following conditions:

- accuracy of the company’s representations and warranties

- effectiveness of a resale registration statement covering the resale of the shares to be sold to the investor

- the company’s common stock must be listed on a national securities exchange

- there must be no material adverse effect with respect to the company

- trading of the company’s common stock shall not have been suspended by the SEC or the applicable stock exchange

- the company shall be in material compliance with its covenants contained in the equity purchase agreement

- no law, rule, regulation, injunction, order or decree of any government or court shall have been issued or adopted which prohibits the sale of equity securities by the company

- all documents required to be filed by the company with the SEC shall have been filed

- to the extent any shareholder approval is required under applicable listing rules in order to issue the shares, the company shall have obtained such shareholder approval

- the company must have delivered instructions to the transfer agent to deliver shares to the investor without a restricted legend in connection with each advance

- the company cannot have filed for bankruptcy

- the company must have reserved the maximum number of shares necessary to issue to the investor

- the investor must have received a legal opinion and 10b-5 letter from company counsel

Some equity purchase agreements also provide that the investor may terminate the agreement upon the occurrence of some or all of the following termination events:

- a material adverse effect with respect to the company occurs

- certain change of control events with respect to the company occur

- the company defaults under the equity purchase agreement or registration rights agreement in a material respect

- the registration statement is not available for a specified period of time (eg, 30 or 45 consecutive trading days, or 90 or 120 trading days within any 365 day period)

- trading in the company’s common stock is suspended for a specified period of time (eg, 3 or 5 consecutive trading days)

The equity purchase agreements typically specify that the company may not issue to the investor shares in an amount greater than 19.99% of the company’s common stock outstanding immediately prior to the execution of the purchase agreement, unless the company’s shareholders have approved the issuance or the issuance exceeds a specified minimum price in accordance with NYSE or Nasdaq rules. This provision is aimed at making sure that shareholder approval is not required under the NYSE and Nasdaq listing rules which require shareholder approval prior to the issuance of 20% or more of the company’s common stock in a private placement. This shareholder approval requirement does not apply to foreign private issuers (although Nasdaq requires a notice that the company will not be complying with the requirement).

The equity purchase agreements generally also provide that, in order to make sure that the investor does not become a 5% holder subject to the Schedule 13D / 13G reporting requirements, the company may not sell shares under the agreement that would result in the investor beneficially owning more than 4.99% of the outstanding shares. Some agreements instead provide a 9.99% cap, or allow the investor to increase the cap from 4.99% to 9.99% of the outstanding shares of the company’s common stock - this would ensure that the investor does not become a 10% holder subject to the reporting and short-swing profit recovery provisions of Section 16 of the Securities Exchange Act of 1934.

The agreements generally include a maximum amount of shares which can be issued by the company in any day, typically characterized as a dollar amount and/or a percentage of the common stock’s trading volume. Examples of caps include the following:

- One agreement’s cap was $1.5 million, subject further to 30% of the average daily trading volume of the common stock over the five consecutive trading days immediately prior to the notice date.

- One agreement imposed a cap of $5 million.

- One agreement imposed a cap of $5 million, subject to the lesser of (a) 100% of the average daily trading volume of the common stock for five trading days before the advance purchase date and (b) 20% of the daily trading volume in the common stock on the purchase date.

- One agreement imposed a daily cap of $20 million, with a further cap of 150% or 50% (depending on the discount to VWAP selected) of the average trading volume of the common stock during the three days before an advance notice.

- One agreement imposed a cap of $25 million, subject to (i) 100% of the average daily trading volume in the common stock for the five consecutive trading days ending before the purchase date and (ii) 20% of the daily trading volume in the common stock on the purchase date.

- One agreement’s cap varied based on the VWAP option chosen – either the lesser of $20 million and 20% of the average daily trading volume during the 5 trading days before the purchase date, or the lesser of $30 million and 40% of the average daily trading volume during the 5 trading days before the purchase date.

- Another agreement imposed a daily cap of $50 million.

Some agreements impose limits on black-out periods during which the investor may not sell shares. One deal provided that no blackout period could exceed 45 days; another imposed a 60 day cap. One deal imposed a limit of 60 consecutive days, or 120 day days, in any 12-month period. The company also may not submit advance notices during a blackout period.

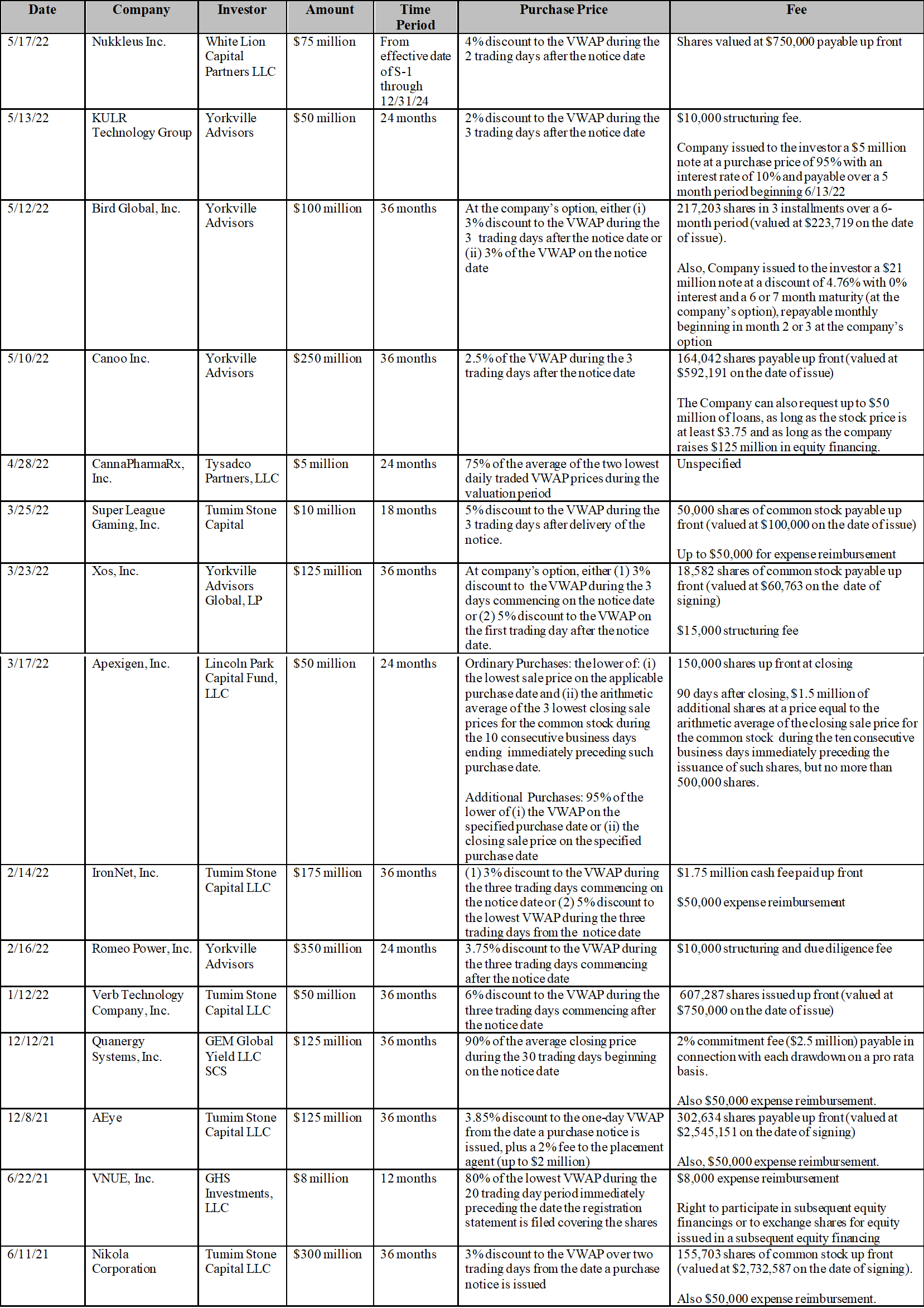

We have included below a link to a chart describing some of the basic terms of recent equity lines of credit.

{kind=link}